Canada Housing & Interest Rate Forecasts for 2026 | Buyer & Mortgage Outlook

Canada’s housing market is poised for a cautious recovery in 2026. Explore expert forecasts on home prices, sales activity, and interest rates — and learn what buyers and mortgage borrowers should expect in the year ahead.

1/5/20262 min read

Canada Housing & Interest Rate Forecasts for 2026 | Buyer & Mortgage Outlook

As we enter 2026, Canada’s housing market is showing signs of recovery, but with important nuances that every potential homebuyer, seller, or mortgage borrower should understand. After a period of high borrowing costs and low sales activity, many economists, real estate firms, and analysts are forecasting a more balanced — yet still measured — market ahead. (MortgageRatesNews.ca)

Moderate Recovery in Home Sales and Prices

According to industry forecasts:

Home sales are expected to rise: The Canadian Real Estate Association (CREA) projects around 509,479 homes will sell in 2026, a +7.7% increase from the previous year — the strongest sales activity since 2021. (GlobeNewswire)

Price growth likely remains moderate: CREA also forecasts the national average home price to grow about 3.2% in 2026 to roughly $698,622, suggesting modest appreciation rather than sharp increases. (GlobeNewswire)

Royal LePage echoes this sentiment, projecting a ~1% price increase by Q4 2026, reflecting improved affordability and supply conditions. (MortgageRatesNews.ca)

However, RE/MAX Canada expects slightly lower average national prices, underscoring regional variation and lingering buyer caution. (MortgageRatesNews.ca)

📌 Key takeaway: More activity and modest price growth are expected, but the pace varies across regions and market segments. (MortgageRatesNews.ca)

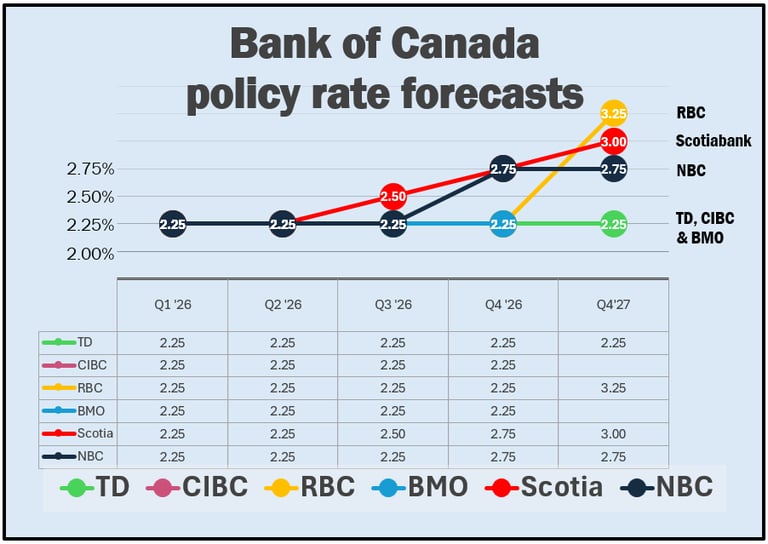

Interest Rate Outlook: Stability, Not Sharp Drops

One of the biggest drivers of housing sentiment is borrowing costs. After several rate cuts in 2024 and 2025 that helped stabilize markets, most forecasts now expect interest rates to stay relatively steady through 2026:

Economists widely predict the Bank of Canada’s policy rate to hover near ~2.25% through most of 2026 — signaling a hold pattern rather than further easing or cuts. (MortgageRatesNews.ca)

Some major banks foresee the possibility of a slight rise in late 2026, while others see rates unchanged through 2027. (MortgageRatesNews.ca)

This suggests relief from the highest borrowing costs of previous years, but no dramatic drop — meaning mortgage payments and renewals may still challenge some borrowers. (MortgageRatesNews.ca)

📌 What this means for borrowers: While mortgage affordability has improved from the height of the rate hiking cycle, most rate relief has already occurred — and future movement may be limited. (MortgageRatesNews.ca)

Regional Differences and Market Dynamics

Canada’s housing market isn’t uniform — economic and supply conditions vary significantly across provinces and cities:

High-demand urban markets like parts of Ontario and B.C. may continue facing affordability constraints, even as sales tick up. (Norada Real Estate)

Smaller and more affordable markets could benefit from increased buyer interest and steady price gains. (Norada Real Estate)

Supply constraints — especially new construction — continue to influence market balance and price trends. (MortgageRatesNews.ca)

📌 Insight: Regional analysis is crucial — what’s true for one city may not hold for another. (Norada Real Estate)

What This Means for You in 2026

Here are the key points Canadian mortgage consumers and homebuyers should know:

✅ Sales activity expected to grow, offering more choice to buyers. (GlobeNewswire)

✅ Home price gains likely moderate, not explosive. (GlobeNewswire)

✅ Interest rates likely stable, meaning planning is key — not hoping for big rate cuts. (MortgageRatesNews.ca)

✅ Regional variations matter more than ever — local trends could outperform or lag national averages. (Norada Real Estate)

Tips for Buyers & Borrowers

Start mortgage planning early: With rate stability likely, you’ll want to lock in terms that match your financial goals. (True North Mortgage)

Look beyond national averages: Investigate local inventory, pricing, and economic conditions. (Norada Real Estate)

Consider future renewals: For existing homeowners, renewals may occur in a higher rate environment than your original loan — plan ahead. (True North Mortgage)

Work with professionals: Mortgage advisors and real estate experts can tailor strategies to your situation.